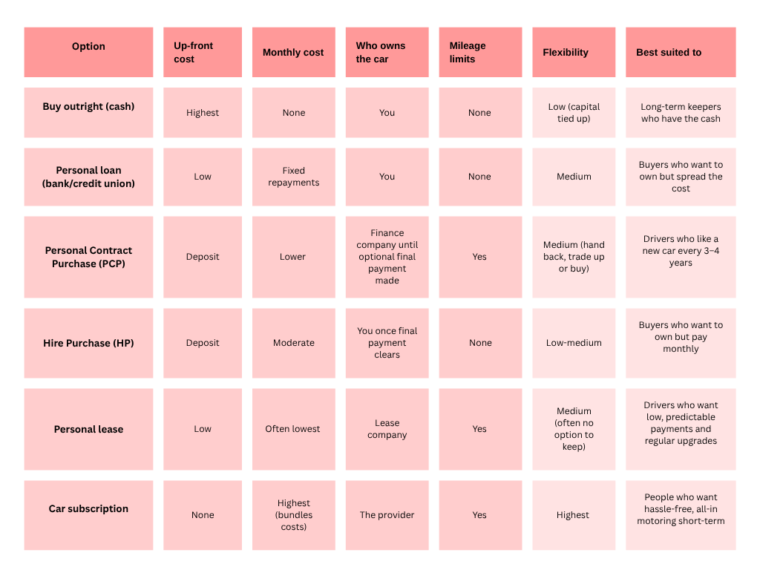

For most Irish drivers, buying is cheaper over the long run and builds equity, while leasing keeps monthly payments and up-front costs low but you never own the car. If you keep cars for years and drive high mileage, buying outright (cash or a credit-union/bank loan) usually wins. If you'd rather change car every few years, want predictable monthly costs and don't mind mileage limits, a personal lease, PCP or subscription can make more sense. The right answer depends on how long you'll keep the car, your annual kilometres, and whether ownership matters to you.

Should you buy your next car outright, take finance on it, or lease it? It's one of the most common questions Irish buyers ask, especially around the January and July plate changes, and there's no single right answer. Below is a side-by-side comparison of every option, how to work out the true cost, and who each one actually suits.

Your financing options at a glance

Whichever route you choose, up-front cost, mileage limits and who ends up owning the car are the three factors that separate them.

What is car leasing, and how does it work in Ireland?

Car leasing means paying a fixed monthly amount to use a car for an agreed term, typically two to four years, after which you hand it back. As a private buyer, leasing was once the preserve of big fleets and company-car schemes, but personal leasing is now widely available in Ireland. Unlike a loan or Hire Purchase (HP), there's usually no option to own the car at the end, and the contract sets an annual mileage limit.

Aren't PCP and HP already a form of leasing?

In many ways, yes. A lot of us are effectively leasing our cars when we think we're buying them. The widely-used PCP (Personal Contract Purchase) is in many ways a lease with an option to buy at the end of the contract. That's why PCPs come with maximum-mileage limits and condition requirements, stipulations many people overlook when they sign. The expectation is that you'll hand the car back at the end of the three or four year term and roll your "purchase" into a new car and a fresh set of monthly payments.

Here's the part few providers state plainly: on a strict legal level, you never actually own a car you're paying for on PCP, you're paying to use it. Your name is on the logbook, but you only fully own it if you pay the "optional final payment" at the end. That final payment cuts both ways: it guarantees the car's future value for you, but it also guarantees the dealer a valuable asset to reclaim if you walk away.

Personal leasing: how it works, and the pros and cons

So why not cut out the middleman and go for a personal lease? The main draw is value: monthly payments on a private lease are often lower than the repayments on a PCP, a Hire Purchase agreement, or a personal loan. Deposits tend to be lower too, and there's no balloon payment to worry about. Many lease plans can also bundle in servicing, maintenance and even tyre replacement, though that advantage has narrowed as PCP and HP packages increasingly offer the same extras.

Pros of leasing

- Lower monthly payments and lower up-front cost than most finance

- No balloon/optional final payment to fund

- Insulates you from swings in used-car resale values

- Servicing and maintenance can often be included

- Easy to upgrade to a newer car at the end of the term

Cons of leasing

- You never own the car and usually can't buy it

- Annual mileage is capped, with excess-mileage charges if you go over

- Wear-and-tear beyond "fair" condition is chargeable at the end

- Ending a lease early can be expensive

- Model, spec and colour choice is often limited

- Usually an online purchase, with little chance to try the car first

A few mechanics worth understanding before you sign: leases set an annual mileage limit (often quoted in kilometres) and charge a per-kilometre excess fee if you exceed it; they include a fair wear-and-tear standard, and damage beyond it is billed at hand-back; and early termination typically triggers a settlement fee. On cost, lease payments aren't usually tied to interest-rate movements the way a variable loan is, but when the lease company's own funding costs and inflation rise, new lease prices tend to rise too. Most PCP and HP deals, by contrast, are sold at a fixed rate, so the monthly cost shouldn't move once you've signed.

Leasing vs hire purchase: what's the difference?

The core difference is ownership. With HP, you pay a deposit and fixed monthly instalments, and the car becomes yours once the final instalment clears, there are no mileage limits and no hand-back. With a personal lease, you never own the car: you return it at the end of the term, you're held to a mileage cap, and you may face excess-mileage or wear charges. HP suits buyers who want to own but pay monthly; leasing suits those who prioritise low payments and a regular upgrade over ownership.

Car subscriptions: a newer, more flexible option

Many carmakers now offer something different again through their dealerships: car subscriptions. Once only trialled here and there, subscriptions have become a more established option in Ireland. They offer a no-deposit, single monthly payment covering the car, motor tax, insurance, maintenance, everything but the fuel you put in or the electricity you charge with. As with a lease, you'll never own the car, but a subscription can be more flexible: you can often upgrade more regularly, or swap a small economy model for something bigger for an occasional weekend or holiday trip.

When buying outright makes the most sense

If you're the kind of buyer who likes to own the car outright and keep it for years, the best route is usually a personal loan from a bank or credit union. Shop around for the best rate, never borrow more than you can comfortably repay, and you'll own the car from day one - no mileage caps, no condition worries beyond your own standards.

If you prefer a new registration on the driveway every few years, PCP or HP still work well: lower monthly costs than a personal loan, usually at fixed rates, just keep the optional final payment on a PCP in mind, and remember it isn't an outright purchase until the last cent is paid. Leasing, meanwhile, suits drivers who want a regular upgrade and painless motoring and aren't too precious about the exact car or spec.

There's one modern wrinkle worth weighing, and it involves electric cars. EV technology is still moving quickly, so buying a current EV outright could, and we're speculating, leave you owning a car that's been overtaken by newer range and charging tech in a few years. For EVs specifically, leasing or PCP can hedge that risk by letting you hand the car back and move on. It's one more factor for the homework.

How to work out the true cost

The mistake most people make is comparing monthly payments alone. To compare fairly, work out the total cost over the same period (say three years) for each route, then factor in what you're left with at the end.

Illustrative figures - swap in a real quote for your own car:

- Buy with a credit-union loan: €0 deposit + (€350 × 36 months) = €12,600. After three years you own a car worth, say, €11,000. True cost is €1,600, plus you keep an €11,000 asset.

- PCP: €3,000 deposit + (€290 × 36) = €13,440 paid. Hand it back and you're done - true cost is €13,440, and you own nothing. Pay the ~€9,000 optional final payment and you own the car, but total outlay rises to ~€22,440.

- Personal lease: €1,050 initial rental + (€300 × 36) = €11,850. Nothing to sell at the end, no equity - true cost is €11,850, plus any excess-mileage or wear charges.

Then add the running costs common to every route, insurance, motor tax, servicing, and the NCT once the car is four years old, and, if you're importing, VRT. The headline monthly figure rarely tells the whole story.

Who should buy, and who should lease?

There's no universal winner, it comes down to how you use a car and what you value:

- Buy outright (cash or credit-union/bank loan) if you keep cars for years, drive high mileage, or want to own an asset free of mileage caps. Cheapest over the long run.

- Choose PCP or HP if you want a newer car every few years with lower monthly costs. HP if ownership matters, PCP if flexibility does (mind that final payment).

- Lease if you want the lowest, most predictable payments, don't care about owning, and stay within a set mileage.

- Subscribe if you want short-term, all-in, hassle-free motoring and maximum flexibility, and don't mind paying a premium for it.

Whichever way you lean, doing your homework on the specific car, its history, valuation and running costs, matters more than the finance label on the contract.

Before you buy, check for outstanding finance

One last piece of homework, and it's the most important. If you're buying a used car privately or taking over someone's PCP or HP, the finance company, not the seller, may still legally own part or all of it until that agreement is cleared. Buy a car with outstanding finance on it and, in the worst case, the debt follows the car and you could lose it. A car history check flags any outstanding finance on a vehicle before you hand over a cent, alongside its full history, so you know exactly what you're buying and who really owns it.

Frequently asked questions: Leasing vs Purchase

Is it better to buy or lease a car in Ireland?

Buying is generally cheaper over the long term and leaves you owning an asset, while leasing keeps monthly and u p-front costs lower but you never own the car. High-mileage, long-term keepers usually favour buying; drivers who upgrade often and want predictable payments favour leasing.

What are the pros and cons of leasing a car?

Pros: lower monthly and up-front costs, no balloon payment, often includes servicing, and easy upgrades. Cons: you never own the car, mileage is capped with excess charges, wear-and-tear is chargeable, and ending early is costly.

How do I work out whether leasing or buying is cheaper?

Compare the total cost over the same period, not just the monthly figure, add every payment, then subtract what the car is worth to you at the end (resale value if you buy, nothing if you lease). See the worked example above.

What's the difference between leasing, Personal Contract Purchase (PCP) and hire purchase (HP)?

With HP you own the car once the final instalment is paid, with no mileage limits. With PCP you only own it if you pay the optional final payment, and mileage is capped. With a lease you never own the car and always hand it back within a mileage limit.

What is car leasing, and does it include insurance?

Car leasing is paying a fixed monthly amount to use a car for a set term before returning it. Leases often bundle servicing and maintenance, but you usually arrange your own insurance and motor tax, car subscriptions are more likely to include insurance. Always check exactly what a contract covers.

by

by